Don’t worry it’s just a wholesale tax not a retail tax…yea right.

Summary

Michigan’s new 24% wholesale cannabis tax is officially moving forward after a Court of Claims ruling that refused to put the brakes on the law. The decision doesn’t settle the underlying constitutional fight, but it does lock in the tax’s January 1 launch and reshapes the financial landscape for growers, processors, and vertically integrated operators.

Background

The tax emerged from Michigan’s 2025–26 budget package—a sweeping fiscal plan that tucked in a cannabis‑specific wholesale levy aimed at generating hundreds of millions for road and infrastructure projects. Almost immediately, industry groups challenged the law, arguing that it effectively rewrites the Michigan Regulation and Taxation of Marihuana Act (MRTMA), the 2018 voter initiative that legalized adult‑use cannabis.

Their argument hinges on MRTMA’s unusually strong amendment protection: any legislative change requires a three‑fourths supermajority. Lawmakers passed the wholesale tax with a simple majority, prompting plaintiffs to claim the Legislature sidestepped the constitutional guardrails voters put in place.

Judge Sima Patel wasn’t persuaded—at least not enough to halt the tax while the case proceeds. Her ruling emphasized that the challengers had not shown a likelihood of success at this early stage and that delaying the tax would disrupt state revenue planning.

Opinions

Industry Viewpoint Operators describe the tax as a blow delivered at the worst possible moment. Wholesale prices have been sliding for years, and many growers are already operating on razor‑thin margins. A 24% levy on transfers—especially internal transfers within vertically integrated companies—could force businesses to raise prices, consolidate, or close. Some argue the tax contradicts MRTMA’s intent to keep legal cannabis competitive with the illicit market.

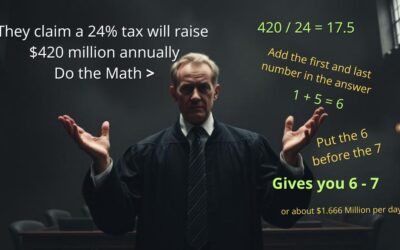

State Viewpoint The state counters that MRTMA’s 10% excise tax applies only to retail sales and does not prohibit additional taxes. In the state’s view, the wholesale tax is a separate fiscal mechanism, not an amendment to MRTMA. Officials also stress the public benefit: the tax is projected to generate roughly $420 million annually for infrastructure, a politically popular use of cannabis revenue.

What’s at Stake

-

The Boundaries of Voter‑Initiated Law Michigan’s constitution gives voter‑approved statutes unusual protection. This case could define how far lawmakers can go without triggering the supermajority requirement.

-

The Future Shape of the Cannabis Market If the tax accelerates consolidation, Michigan could see fewer independent operators and more dominance by large, multi‑location companies.

-

Consumer Pricing and Illicit Market Competition Higher wholesale costs may ripple into retail pricing, potentially widening the gap between legal and illicit products.

-

State Budget Stability If the tax is later struck down, Michigan could face a significant revenue shortfall and a scramble to fill the gap.

In The End

The ruling is not a final word—it’s the opening chapter. The constitutional question remains alive, and the case will move forward with full briefing and likely appeals. But for now, the tax is real, the clock is ticking, and Michigan’s cannabis industry must adapt to a new economic reality while the courts decide how much power the Legislature truly has over a voter‑created regulatory system.

FAQs

Q: When does the 24% wholesale tax take effect?

A: It is scheduled to begin on January 1, following the judge’s refusal to pause the law.

Q: Does this tax apply to transfers within the same company?

A: Yes. Vertically integrated businesses must apply the tax to internal wholesale transfers.

Q: Is this tax considered an amendment to MRTMA?

A: That is the core dispute. The state says no; industry plaintiffs say yes. The court has not ruled on the merits yet.

Q: Could the tax still be overturned?

A: Yes. The judge’s ruling only denies a temporary block. The constitutional challenge continues.

Q: How much revenue is the state expecting from the tax?

A: Approximately $420 million annually, largely earmarked for road and infrastructure projects

Relevant Laws and Cases

-

Michigan Regulation and Taxation of Marihuana Act (MRTMA)

-

Michigan Constitution, Article II, § 9

-

Michigan Court of Claims

-

League of Women Voters v. Secretary of State (2018)

-

Michigan Budget Acts and Fiscal Legislation

Here’s another briefing

CANNRA Briefing on Schedule III – December 18 2025

Here’s something else

Michigan gets a new state budget: Winners, losers in the $81B deal

And now for something completely different

- Minnesota SCAM (Google Search)

- A little fraud never hurt anyone? (DOJ).

- News Releases | ICE – What’s going on?

- DOGE: What are they doing?

- National Health Care Fraud Takedown Results in 324 Defendants Charged in Connection with Over $14.6 Billion in Alleged Fraud.

- Judge’s Ruling Clears Way for Michigan’s New 24% Percent Wholesale Tax on Cannabis

As always… Follow the money.

More Posts

Florida Rejects 2026 Petition for Adult‑Use Marijuana

Florida officials say no citizen‑initiated amendments—including a major recreational marijuana...

Oops-We Taxed You Again-Proposed 32% Tax on Internet Devices for Kids

Michigan’s proposed 32% sin device tax on top of convience fees, service fees, credit card fees,...

Michigan judge and 3 others charged in stealing from incapacitated adults

Detroit Judge Accused of Joining Scheme to Drain Funds From Incapacitated AdultsSummary A Detroit...

The Cannabis Shift Show

The Cannabis Shift Show. Michigan is leaving its “green rush” phase and entering a period of...

How Ohio’s $1B Cannabis Boom Impacts Michigan

Michigan vs. Ohio: The Cannabis Shift Show. Ohio Hits $1 Billion in "Legal" Marijuana Sales in...

Court Allows Challenge to Michigan’s New 24% Cannabis Tax

Summary In Michigan cannabis news a Michigan Court of Claims judge has ruled that the lawsuit...