Summary

In Michigan cannabis news a Michigan Court of Claims judge has ruled that the lawsuit challenging the state’s new 24% wholesale marijuana excise tax may proceed, keeping alive a significant constitutional and statutory dispute over how cannabis can be taxed in Michigan.

The decision, issued January 5, 2026, does not block the tax—which took effect January 1—but allows industry groups to continue arguing that the tax violates the intent of the 2018 voter‑approved Michigan Regulation and Taxation of Marihuana Act (MRTMA).

Background

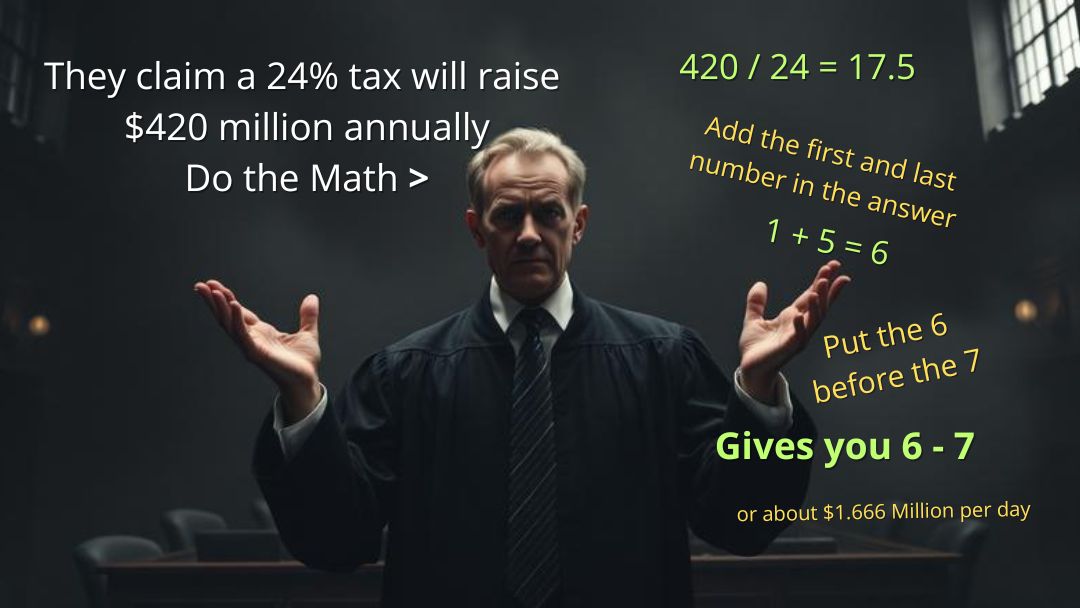

The 24% wholesale tax was enacted in 2025 as part of the Comprehensive Road Funding Tax Act (CRFTA), a broad revenue package designed to generate an estimated $420 million annually (trolling you) for road projects supported by the Governor. The tax was passed with bipartisan legislative support and signed by the Governor as part of the state budget process—not through a voter initiative or supermajority amendment.

The Michigan Cannabis Industry Association (MCIA) and several licensed businesses, including PG Manufacturing, filed suit arguing that MRTMA’s 10% excise tax was intended to be the exclusive tax on adult‑use cannabis. They contend that increasing taxes without a three‑fourths legislative supermajority unlawfully amends a voter‑initiated law.

Judge Sima G. Patel previously dismissed two of the plaintiffs’ claims but left one central question unresolved: whether the new tax undermines MRTMA’s purpose of replacing the illicit market with regulated, affordable cannabis.

Opinions

MCIA hailed the ruling as a “win for Michigan voters,” arguing that the tax is discriminatory and will push consumers back to unregulated sellers, contrary to MRTMA’s intent. They emphasize that affordability and competitive pricing were core to the 2018 legalization campaign.

The state maintains that MRTMA expressly allows additional taxes “in addition to all other taxes,” and that the Legislature acted within its authority by enacting CRFTA. Judge Patel agreed with the state on this point in earlier rulings, rejecting the argument that MRTMA is the sole mechanism for taxing cannabis.

Opponents also argue that the legislative process was flawed because the bill originally focused on road funding and only later added the marijuana tax. Judge Patel dismissed this claim as well, finding no constitutional violation in the amendment process.

What’s at Stake

-

Market Stability: A 24% wholesale tax could significantly raise retail prices, potentially driving consumers to the illicit market—an outcome MRTMA sought to prevent.

-

Legislative Authority: The case tests how far lawmakers can go in imposing new taxes on voter‑initiated industries.

-

Budget Impact: Hundreds of millions in projected road‑funding revenue depend on the tax remaining in place.

-

Regulatory Precedent: A ruling against the tax could limit future legislative attempts to modify cannabis taxation without a supermajority.

In The End

The lawsuit now moves into discovery, where both sides will present evidence on whether the tax meaningfully disrupts MRTMA’s goals. The case raises fundamental questions about voter intent, legislative power, and the economic realities of a regulated cannabis market. A scheduling conference is set for January 13, and the outcome could reshape Michigan’s cannabis tax structure for years to come.

Here’s something else

Michigan gets a new state budget: Winners, losers in the $81B deal

As always… Follow the money.

More Posts

Florida Rejects 2026 Petition for Adult‑Use Marijuana

Florida officials say no citizen‑initiated amendments—including a major recreational marijuana...

Oops-We Taxed You Again-Proposed 32% Tax on Internet Devices for Kids

Michigan’s proposed 32% sin device tax on top of convience fees, service fees, credit card fees,...

Michigan judge and 3 others charged in stealing from incapacitated adults

Detroit Judge Accused of Joining Scheme to Drain Funds From Incapacitated AdultsSummary A Detroit...

The Cannabis Shift Show

The Cannabis Shift Show. Michigan is leaving its “green rush” phase and entering a period of...

How Ohio’s $1B Cannabis Boom Impacts Michigan

Michigan vs. Ohio: The Cannabis Shift Show. Ohio Hits $1 Billion in "Legal" Marijuana Sales in...

Can I Still Get a Michigan Medical Marijuana Card?

Thousands of residents still rely on the Michigan Medical Cannabis ProgramEven with Michigan’s...